How Daily Resetting 300% Inverse Leveraged ETNs May Perform in Bull, Bear and Volatile Markets

For those investors that are bearish, certain MicroSectors daily-resetting inverse leveraged Exchange-Traded Notes (ETNs) may offer investors the ability to participate in 300% of the inverse daily return of specific indices, before taking into account fees and expenses. Sophisticated investors that have a bearish view may consider a 300% inverse leveraged daily-resetting ETN to receive a positive gain that is triple the daily loss of the benchmark index. This article provides an overview of how these products perform in different environments.

Inverse leveraged ETNs may be a suitable investment for you if:

- You seek a short-term investment with an upside return linked to a three times leveraged participation in the inverse performance of the applicable index, compounded daily.

- You believe the level of the index will decrease in the short term.

- You understand (i) leverage risk, including the risks inherent in maintaining a constant three times daily inverse leverage, and (ii) the consequences of seeking leveraged investment results generally.

- You are a sophisticated investor, understand path dependence of investment returns and you seek a short-term investment in order to manage daily trading risks.

- You are willing to accept the risk that you may lose some or all of your investment, especially if the level of the underlying index increases.

Inverse leveraged ETNs may not be a suitable investment for you if:

- You believe the level of the index will increase in the short term.

- You do not seek a short-term investment with a downside return linked to a three times leveraged participation in the inverse performance of the applicable index, compounded daily.

- You do not understand (i) leverage risk, including the risks inherent in maintaining a constant three times daily inverse leverage, or (ii) the consequences of seeking leveraged investment results generally.

- You are not a sophisticated investor, do not understand path dependence of investment returns or you seek an investment for purposes other than managing daily trading risks.

- You are not willing to accept the risk that you may lose some or all of your investment.

Hypothetical ETN Performance

The following examples and tables illustrate how daily resetting 300% inverse leveraged ETNs would perform over a period of five trading days in different circumstances. They are intended to highlight how the return on the ETNs is affected by the daily performance of the applicable index, leverage, compounding and path dependency, before product fees and expenses.

The resetting of the leverage on each day is likely to cause each note to experience a “decay” effect, which is likely to worsen over time, and will be greater the more volatile the level of the index. The “decay” effect refers to a likely tendency of the notes to lose value over time. Accordingly, the notes are not suitable for intermediate- or long-term investment, as any intermediate- or long-term investment is very likely to sustain significant losses, even if the index depreciates over the relevant time period. Although the decay effect is more likely to impact the return on the notes the longer the notes are held, the decay effect can have a significant impact on the note performance even over a period as short as two days.

The notes are suitable only for sophisticated investors. If you invest in the notes, you should continuously monitor your holdings of the notes and make investment decisions at least on each trading day.

All the examples assume that the notes were purchased on day 0 at an indicative note value of $50 and disposed of on day five at the applicable indicative note value, and that no market disruption events occurred. For ease of analysis, all values have been rounded to two decimal places, and no product fees or expenses were included in the calculations. (In contrast, an actual exchange traded note will have fees built into the product that would reduce the indicative note value and an investor’s return.)

In each example, the “Note Return” is the change in the Closing Indicative Note Value from Day 0 to Day 5.

Hypothetical Examples

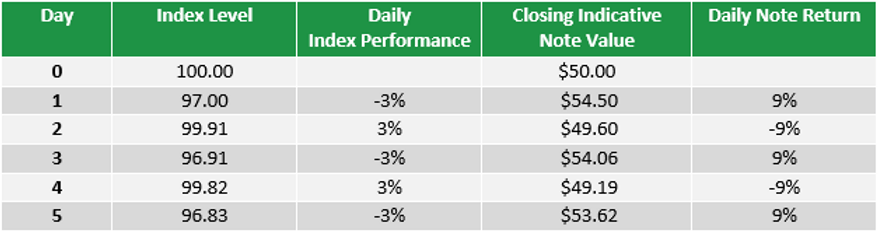

Example #1: The index level alternatively decreases then increases by a constant rate of 3.00% per day, with the index level decreasing by -3.17% by day five and with a note return of 7.24%.

Assumptions

Principal Amount: $50.00

Initial Index Level: 100.00

Note Return: 7.24%

Cumulative Index Return: -3.17%

Final Indicative Note Value: $53.62

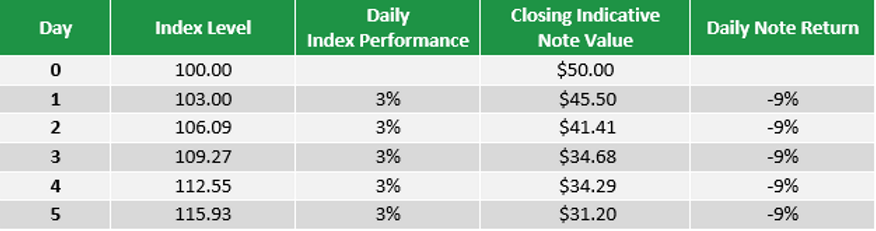

Example #2: The index level increases by a constant 3.00% per day, with the index level increasing by 15.93% by day five and with a note return of -37.60%.

Assumptions

Principal Amount: $50.00

Initial Index Level: 100.00

Note Return: -37.60%

Cumulative Index Return: 15.93%

Final Indicative Note Value: $31.20

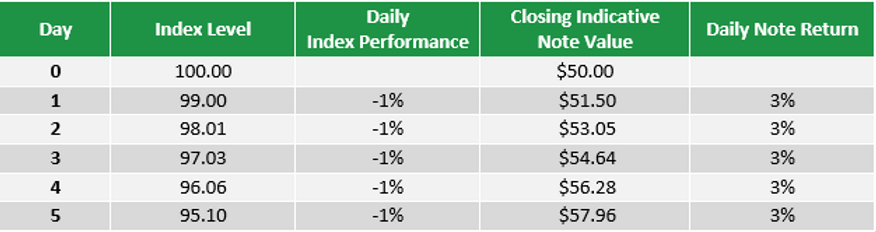

Example #3: The index level deceases by a constant rate of -1.00% per day, with the index level decreasing by -4.90% by day five and with a note return of 15.92%.

Assumptions

Principal Amount: $50.00

Initial Index Level: 100.00

Note Return: 15.92%

Cumulative Index Return: -4.90%

Final Indicative Note Value: $57.96

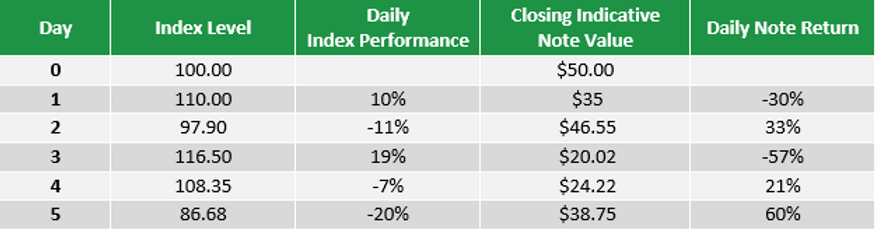

Example #4: The index level decreases in a volatile manner, with the index level decreasing by -13.32% by day five and with a note return of -22.50%.

Assumptions

Principal Amount: $50.00

Initial Index Level: 100.00

Note Return: -22.50%

Cumulative Index Return: -13.32%

Final Indicative Note Value: $38.75

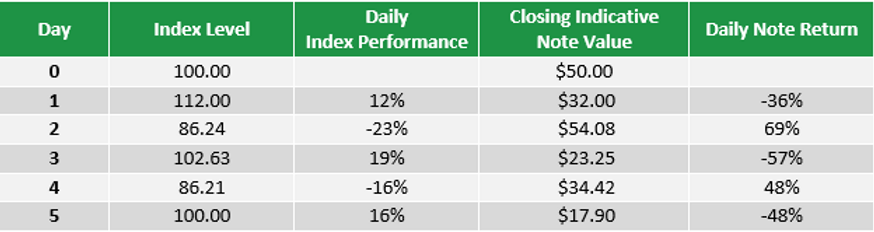

Example #5: The index level increases and decreases in a volatile manner, with the index level ending at the same level.

Assumptions

Principal Amount: $50.00

Initial Index Level: 100.00

Note Return: -64.20%

Cumulative Index Return: 0.00%

Final Indicative Note Value: $17.90

Are Inverse Leveraged ETNs right for everyone?

No – inverse leveraged ETNs are not intended for all investors. Due to the riskiness of these products, the complexity of daily resetting leverage, the nature of path dependency and the fact that these investments are meant to be held for short-term periods, sometimes less than a single day, these investments are not for everyone. Inverse leveraged ETNs are designed to magnify the inverse performance of a particular index on a daily basis. For example, a 300% inverse leveraged daily resetting ETN linked to an index that increases 3% in a single day could potentially result in a 9% loss to investors before fees and expenses. The ETNs are intended to be daily trading tools for sophisticated investors to manage daily trading risks as part of an overall diversified portfolio. Only sophisticated investors who understand daily resetting ETNs and their risks should consider investing.

* * *

Please consider the following additional information about ETNs that is set forth in the links below

Additional Important Information:

Daily resetting inverse leveraged ETNs may underperform in a positive trending performing market, outperform in a negative trending market, and depending on the volatility and index performance in a volatile market, outperform or underperform alternative investment strategies. Accordingly, the notes are not suitable for intermediate- or long-term investment, as any intermediate- or long-term investment is very likely to sustain significant losses, even if the index level decreases over the relevant time period. The notes are suitable only for sophisticated investors. If you invest in the notes, you should continuously monitor your holdings of the notes and make investment decisions at least on each trading day.

The exchange traded notes are subject to the credit risk of Bank of Montreal, the issuer of the ETNs. The ETNs are also subject to the issuer’s credit ratings, and the issuer’s credit spreads may adversely affect their market value.

Inverse leveraged ETNs are intended to be daily trading tools for sophisticated investors to manage daily trading risks as part of an overall diversified portfolio. They are designed to achieve their stated investment objectives on a daily basis. The returns on the ETNs over longer periods of time can, and most likely will, differ significantly from the return on a direct long or short investment in the index. Investors should carefully review the applicable offering documents for an ETN prior to making an investment decision.

Bank of Montreal, which participated in the preparation of this article, and is the issuer of ETNs described on REX’s website, has filed a registration statement (including a pricing supplement, a product supplement, a prospectus supplement and a prospectus) with the Securities and Exchange Commission (the “SEC”) about each of the offerings to which this free writing prospectus relates. Please read those documents and the other documents relating to these offerings that Bank of Montreal has filed with the SEC for more complete information about Bank of Montreal and these offerings. These documents may be obtained without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Bank of Montreal, any agent or any dealer participating in these offerings will arrange to send the applicable pricing supplement, product supplement, prospectus supplement and prospectus if you so request by calling toll-free at 1-877-369-5412.

Recent Posts